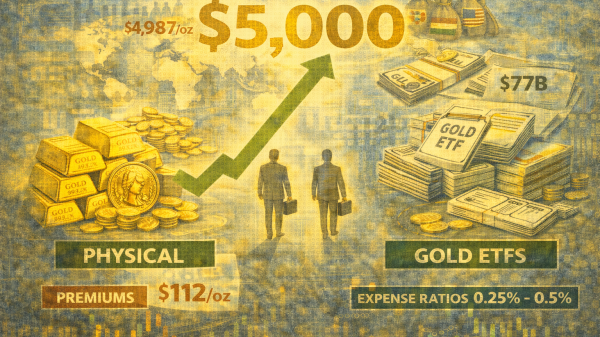

Gold is knocking on the $5,000-per-ounce door after a historic 66% rally in 2025, driven by geopolitical shocks, a weakening dollar, and relentless central bank buying of the precious metal.

The impressive rally has investors reconsidering a critical decision: should they own bullion directly or buy exposure through exchange-traded funds?

The answer depends entirely on what gold means to you in your portfolio.

Spot gold touched nearly $4,987/oz this week, marking an all-time high. The rally has fueled unprecedented demand.

Record-breaking ETF inflows of $89 billion in 2025 signal that investors are increasingly viewing gold as a strategic monetary asset, not just a cyclical hedge.

Yet for those preferring tangible ownership, physical premiums have created new complications.

In India, gold premiums surged to their highest level in a decade, with dealers charging an extra $112 per ounce on top of spot prices as investors rushed to buy ahead of an expected import duty increase in the February budget.

Why gold is charging toward $5,000

The macro forces underpinning gold’s ascent remain intact. Geopolitical uncertainty keeps investors defensive.

The Federal Reserve is expected to cut rates further in 2026, which makes non-yielding assets like gold more attractive.

Most importantly, central banks continue accumulating gold at levels not seen in decades.

Emerging market diversification into bullion reflects a deliberate shift away from dollar dependency, a trend analysts expect to persist.

Nicky Shiels, Head of Research & Metals Strategy at MKS PAMP, called this shift “a new geomacro regime” where gold functions as a strategic monetary asset amid fiscal dominance risks and geopolitical fragmentation.

She projects gold could average $4,500 per ounce in 2026, with upside scenarios reaching $5,400.

JPMorgan’s Natasha Kaneva frames gold as their “highest conviction long,” seeing it hitting $5,055 by late-2026 and potentially $6,000 by 2028.

Physical vs. paper: Trade-offs and who should choose which

When buying physical gold, coins, or bars, expect to pay a retail premium of 5 to 10% above the spot price.

Storage and insurance add another layer of costs, typically running 0.5 to 1% annually or more, depending on security arrangements.

If you buy jewelry, the making charges add another 5 to 20% non-recoverable cost.

In India, physical purchases also carry a 3% sales tax. The upside is complete counterparty risk elimination and tangible ownership.

Gold ETFs like GLD operate differently.

Expense ratios run just 0.25 to 0.50% annually, often cheaper than physical storage and insurance combined.

Trading occurs instantly during market hours. There’s no making charge, no GST burden, and no purity verification concerns.

The trade-off is that you own shares in a fund, not gold itself, introducing minor counterparty risk (though fully backed funds minimize this).

For investors buying gold as an emergency hedge or sovereignty insurance, allocating 5 to 10% of portfolio weight to physical gold in a secured vault makes sense.

For portfolio diversifiers seeking pure liquid exposure, ETFs win on cost efficiency and convenience.

The decision comes down to your objective. If you’re hedging against systemic breakdown, hold some physical.

If you’re building diversification, go with ETFs. Either way, at $5,000 and climbing, ensure your allocation reflects your risk tolerance and time horizon.

The post Gold near $5,000/oz: physical vs. paper- what’s the smarter buy? appeared first on Invezz